On-the-ground research in Indonesia

深入印尼的实地调研

Our user research team conducted on-site interviews in Indonesia — I collaborated closely with them remotely, synthesizing findings into design decisions in real time.

用研同事前往印尼进行实地访谈,我在线上密切配合,实时将调研发现转化为设计决策。

Competitive Landscape

竞品全景

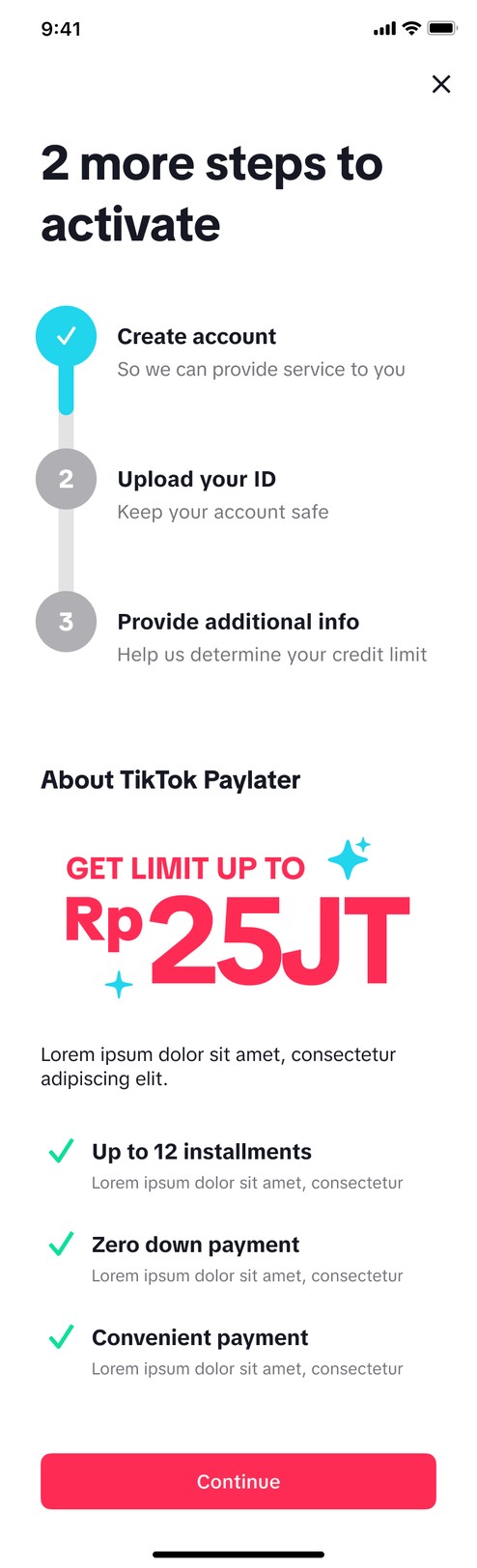

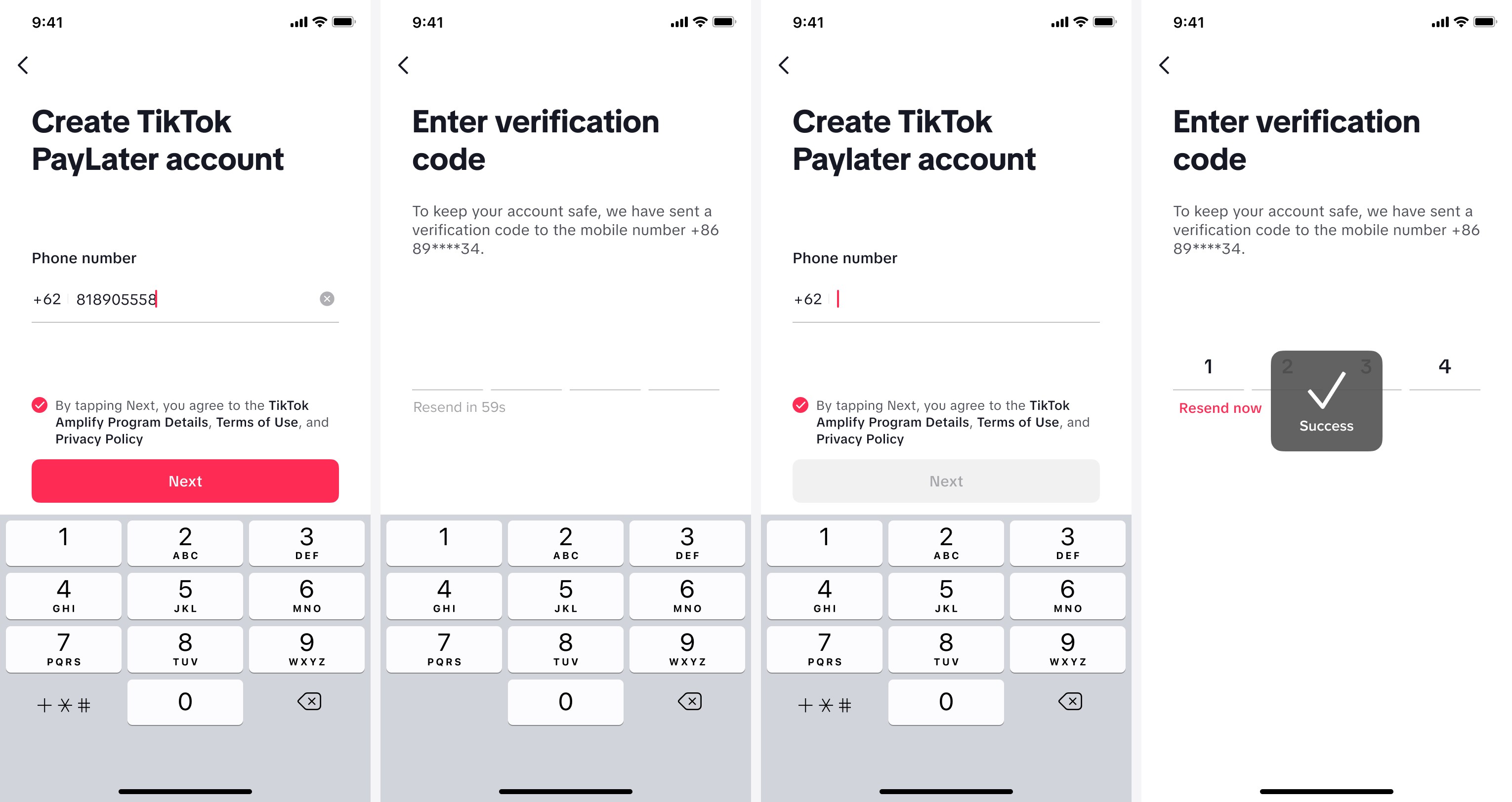

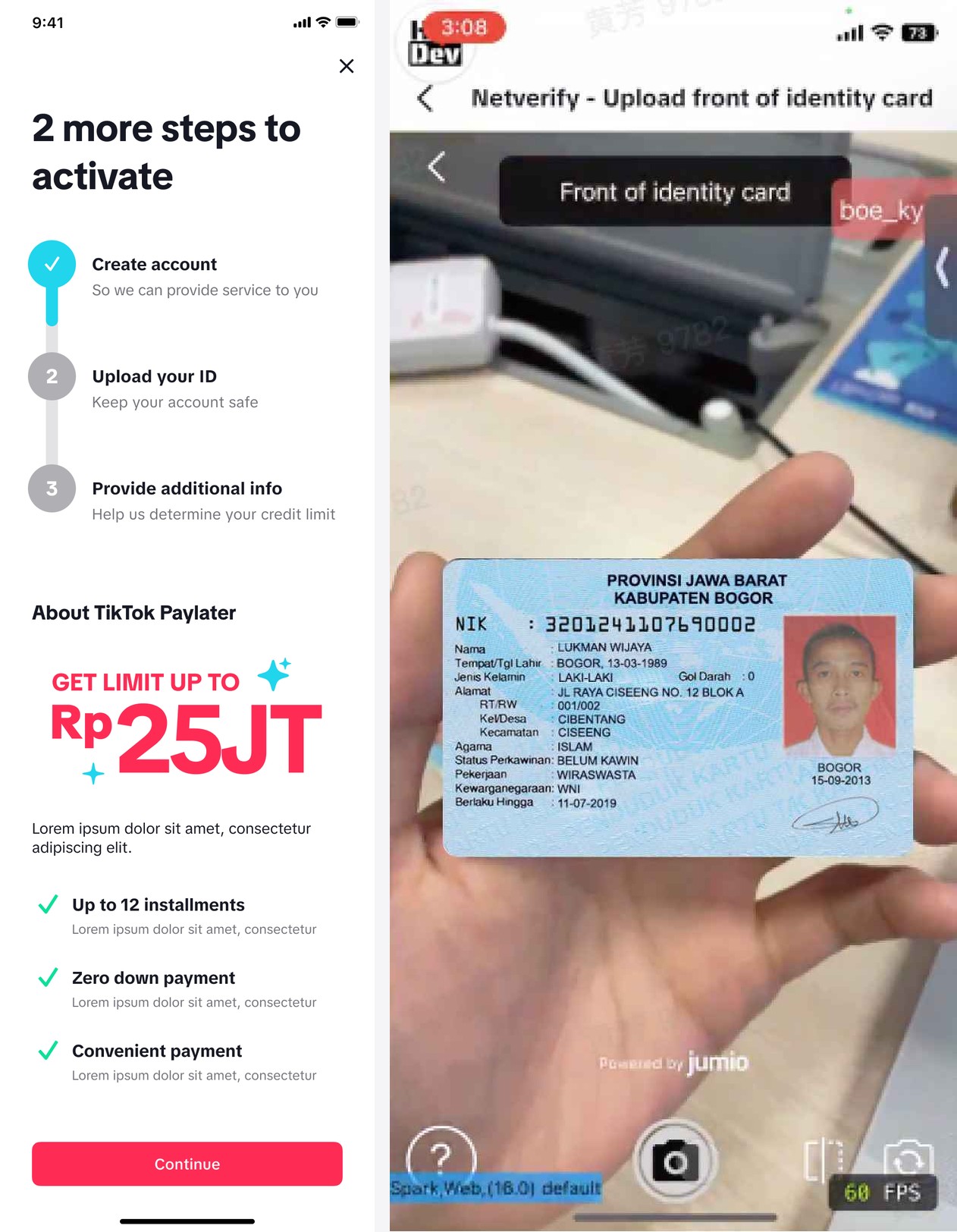

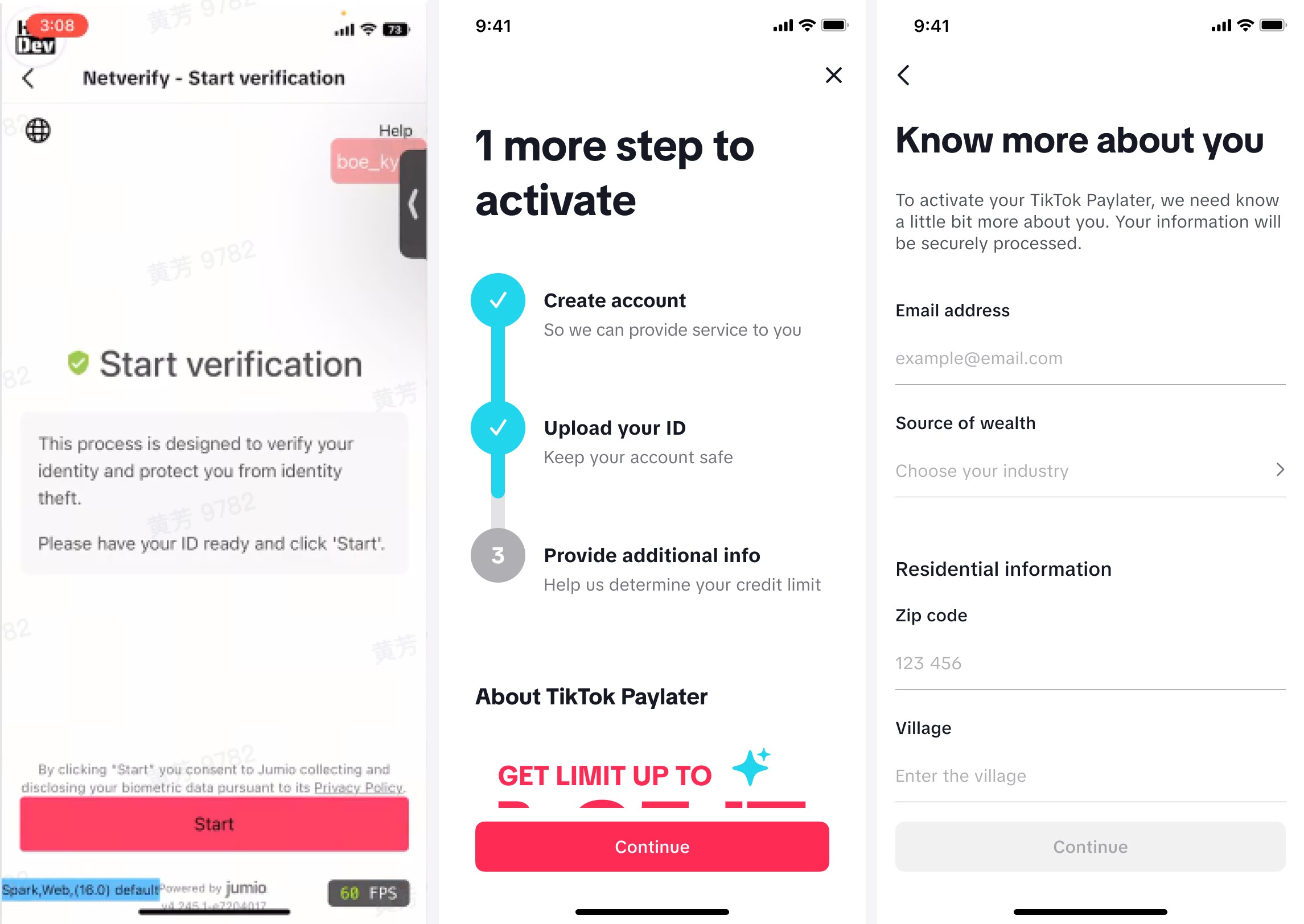

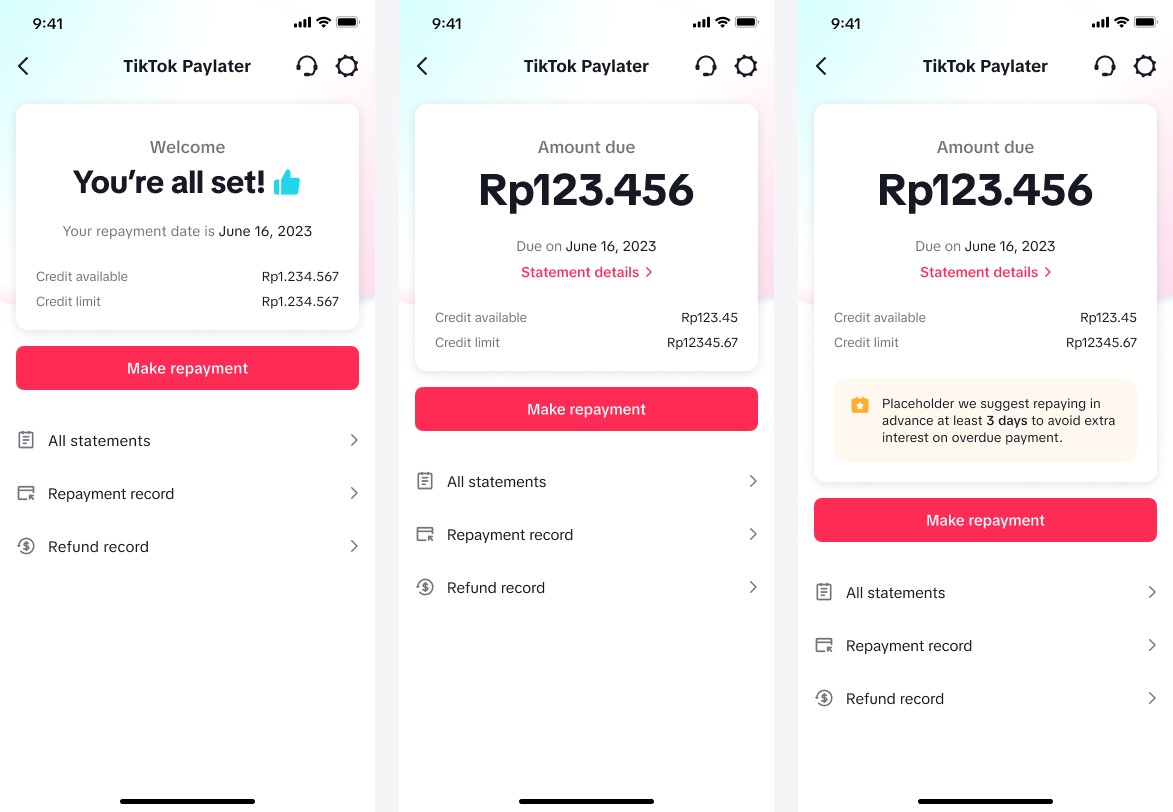

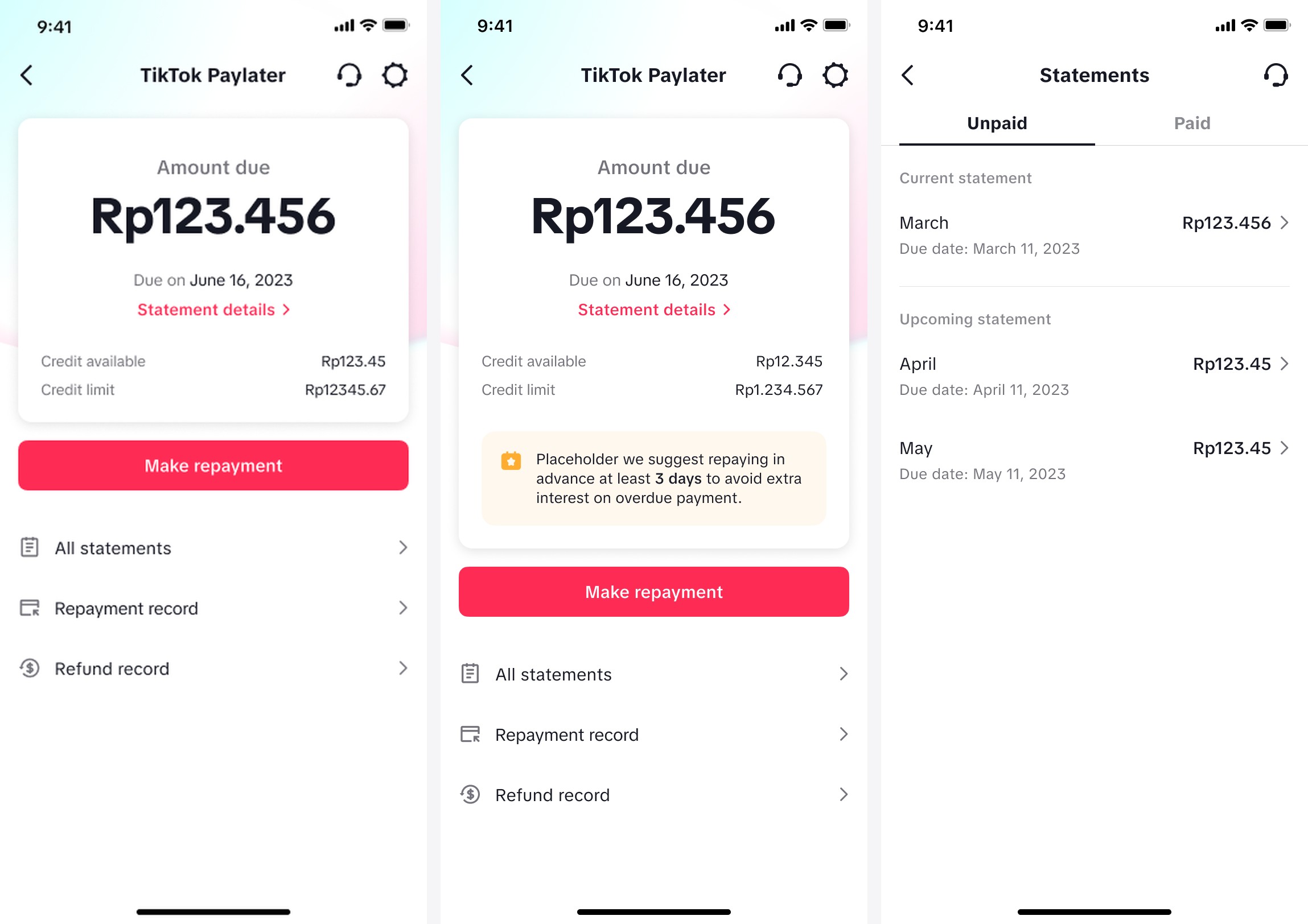

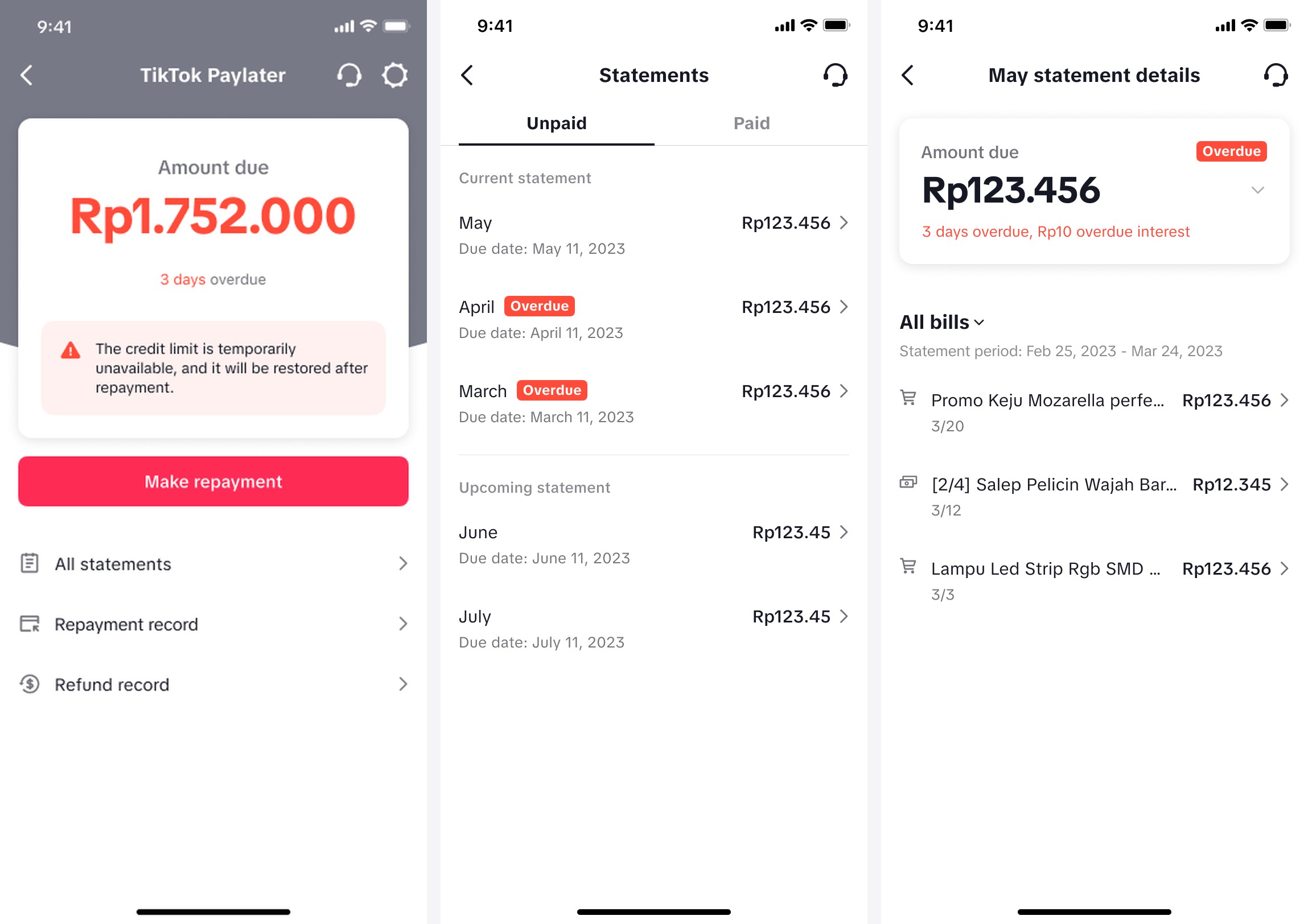

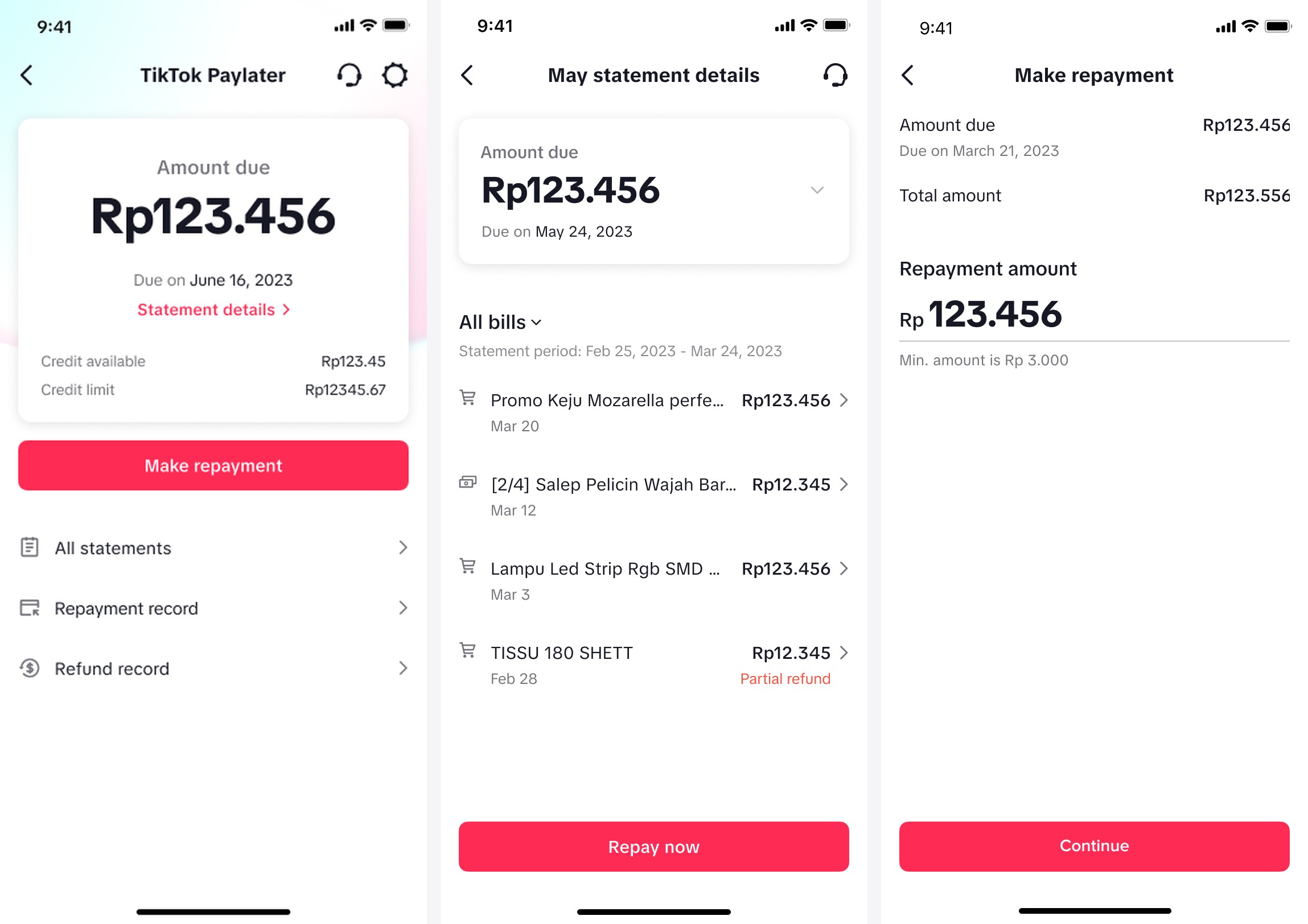

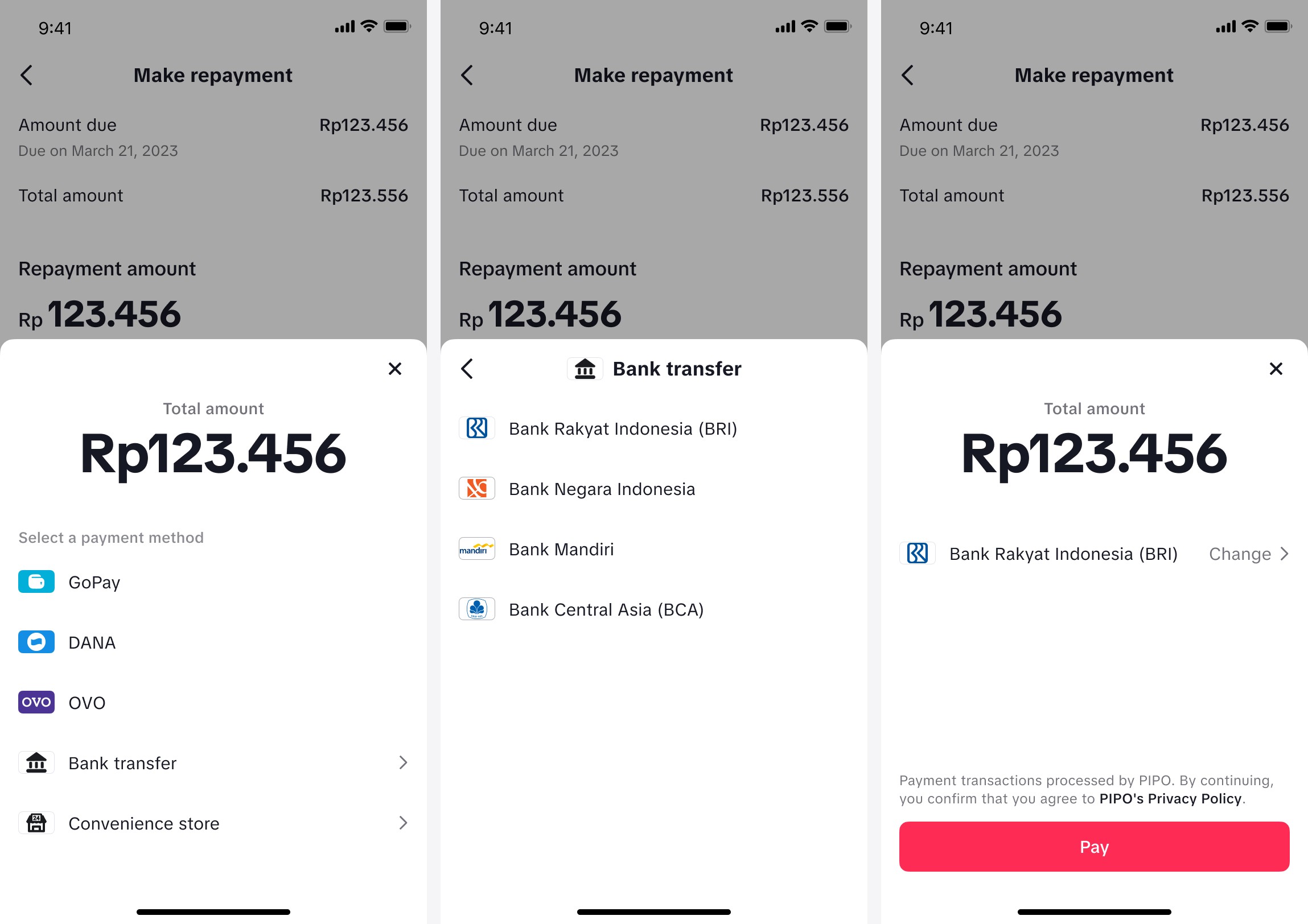

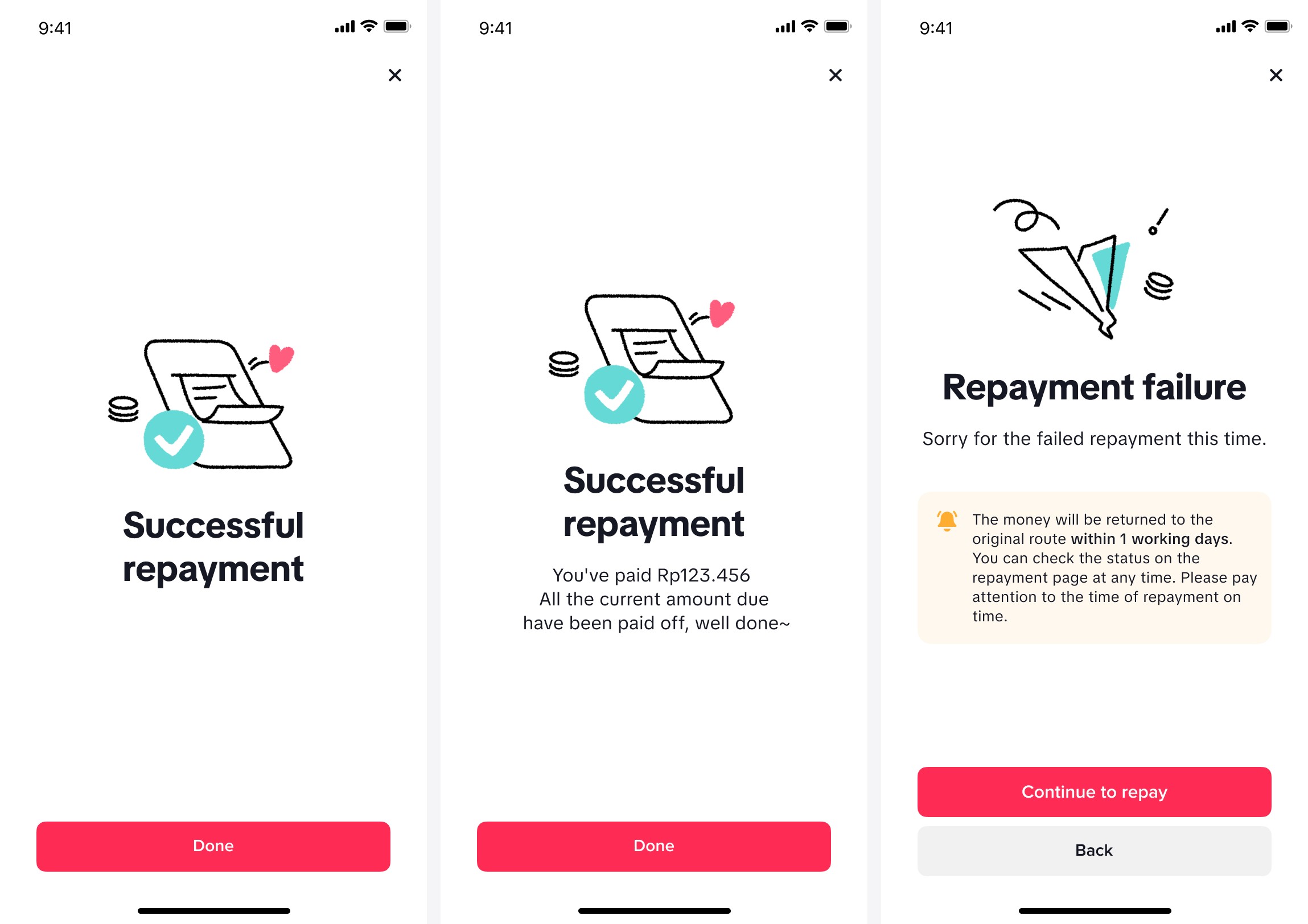

I mapped 6 BNPL products across two axes — e-commerce native vs. third-party lender, and account-level vs. bill-level repayment — then walked through each credit application flow end-to-end to audit field count, KYC method, and drop-off risk.

我系统梳理了 6 款 BNPL 产品,从两个维度建立坐标系:电商自营 vs. 第三方品牌、账户维度还款 vs. 账单维度还款。随后逐一走查每款产品的授信申请全流程,重点审计字段数量、KYC 方式与流失风险节点。

Step labels hide actual field count — users don't see the full form length upfront. Shortest perceived application in the set.

步骤标签遮蔽了真实字段数,用户感知表单最短,同类中开通意愿最高。

Most comprehensive KYC — NIK, selfie, income, employment. PIN set at onboarding and rarely used again; forgetting rate is a known support issue.

KYC 最完整:NIK、自拍、收入来源、工作信息。开通时设 PIN 此后极少使用,遗忘率高是已知客诉。

Checkout-embedded entry minimises context switching. KYC delegated to Kredivo with a mid-flow app handoff — a potential drop-off point.

从结账页直接进入,减少上下文切换。KYC 委托 Kredivo,需跳转第三方 app,存在流失节点。

Reuses existing Grab KYC — existing users skip re-verification entirely. Lowest friction in the set, but locked inside Grab's ecosystem.

复用 Grab 已有 KYC,老用户免重新验证,摩擦最低。但强依赖 Grab 生态,迁移性差。

Most aggressive data collection: blood type, employment history, number of children. The canonical example of how form friction kills conversion.

字段最多:血型、工作经历、子女数量。是「表单摩擦杀死转化率」的典型反面教材,用研中被用户主动提及为放弃原因。

Philippines reference — lighter KYC under a different regulatory environment. Used to understand SE Asia variance, not as a direct model.

菲律宾市场参照,监管不同 KYC 更轻。用于理解东南亚各市场差异,非直接参考对象。

Key Insights from User Interviews

用户访谈核心洞察

-

💡

Brand trust determines adoption. 品牌信任是开通意愿的决定性因素。 Users showed significantly higher willingness to apply when BNPL was positioned as the platform's own product. TikTok's existing brand credibility was an asset to design around. 当 BNPL 以平台自有品牌呈现时,用户开通意愿显著提升。TikTok 的品牌信任度是可以被设计利用的资产。

-

💡

Form length is the primary conversion killer. 表单长度是转化率的主要杀手。 Users recalled abandoning previous BNPL applications when forms felt intrusive — blood type, work history, number of children. 用户反映曾因表单过于繁琐而放弃申请,如血型、工作经历、子女数量等信息让他们感到不适。

-

💡

PIN forgetting is a latent support burden. PIN 遗忘是潜在的客诉定时炸弹。 Users set a PIN once at onboarding and rarely use it. Many forget it by the time a payment is due — and the recovery flow is complex. 用户只在开通时设置一次 PIN,此后鲜少使用,到真正需要还款时往往已遗忘,而找回流程又相当复杂。

-

💡

Phone number recycling is a uniquely SE Asian problem. 手机号二次放号是东南亚特有问题。 Secondary SIM usage is widespread in Indonesia. Abandoned numbers tied to PayLater accounts create dispute and fraud vectors that don't exist in stable-number markets. 印尼二次放号现象普遍,绑定 PayLater 账户的手机号一旦被弃用,既无法被原主人修改,也无法被新持有人使用,极易产生纠纷和客诉。